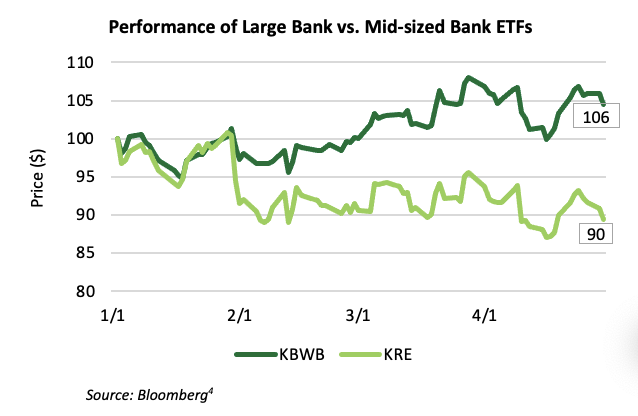

The recent turmoil at New York Community Bank (“NYCB”) has dragged down the stocks of small-to-mid-sized banks again this year. The exchange traded fund for mid-sized banks, the SPDR S&P Regional Banking ETF (“KRE”), underperformed the ETF for large banks, which is the Invesco KBW Bank ETF (“KBWB”) in the 1st quarter. The KRE was down 3.33% while the KBWB was up 10.01%. The underperformance of the mid-sized banks versus the large banks continued in April. Large banks are perceived by investors as having less credit risk, more robust credit reserves, and more liquid balance sheets.

There are obvious headwinds that the banks are facing: tepid loan growth, competitive deposit environment, and an uncertain credit environment; however, we see opportunity in selected small-to-mid-sized regional banks (“SMID banks”). We think stock investors are overly pessimistic in their assessment of SMID bank credit concerns. We believe the larger issues for SMID banks are interest rate risk and loan volume growth. Regarding interest rates, we see banks having a wide disparity of performance based on the positioning of their securities portfolios, their percentage of fixed rate loans, and how they manage their deposit franchise. Many banks have navigated the move in higher rates well and remain well-positioned for the current environment. We also see differences in how banks manage their loan growth. Some banks continue to grow loans and deposits and accept that margins in the near-term are narrower due to the inverted yield curve and competitive deposit environment. We think these banks will be rewarded when the yield curve normalizes, and they realize wider net interest margins on a larger book of business.

Within SMID banks we group our favorites into three buckets: Puerto Rican banks, growth banks, and small banks with unique stories.

Credit Risk

Credit risk is perilous for banks. The current environment poses four areas where banks may experience heightened credit losses. The first area is office buildings. The second area is rent-regulated apartment buildings in New York City. The third is commercial estate properties (“CRE”) where the rapid rise in interest rates has caused the value of CRE to decline. The fourth is rapidly rising debt costs for borrowers with floating rate debt.

So far in the Q1 bank earnings season, banks have reported better than expected credit metrics. The increases in non-performing assets and criticized loans are not alarming given that bank credit metrics were at record lows in 2022 and 2023. We’ll have to remain vigilant about credit risk to see if metrics deteriorate in the coming quarters. In the meantime, we will stay focused on banks with historically strong credit cultures. As we meet with bank management teams, we remain alert for any changes in risk appetites. Many market participants have a negative view of bank managements’ ability to see pending problems in their loan portfolios. We note that risk management and monitoring of loan portfolios has improved from when we started investing in bank stocks. We realize that bank stock investors may need to see the other side of the credit cycle before putting higher multiples on bank stocks and this contributes to the current opportunity we see.

Interest Rate Risk

Market participants are divided on the outlook for banks. Some investors see an opportunity because banks are cheap and poised to benefit from interest rate cuts. Others are concerned about potential credit losses or rising interest rates. We believe selective opportunities exist, with certain banks offering attractive valuations and potential for earnings growth, while others are at risk as they have significant holdings of fixed-rate loans and securities on their books.

Banks benefit from higher reinvestment yields, but some banks have more near-term opportunity. If a bank has a lot of loans and securities maturing in the next year at low yields, they can take the proceeds from the loan payoff to make a new loan at today’s higher yield. Unfortunately, many banks made a lot of 5-year and 7-year fixed-rate loans in 2021 and 2022 that won’t mature until 2026 or as late as 2029.

In a more robust deposit environment, banks would generate loan growth which would allow new production to be put on the books at normalized spreads.

In 2022 and very early 2023, almost all banks paid aggressively low deposit rates even as the Federal Reserve raised the Federal Funds rate. Most bank customers had become accustomed to the zero-interest rate environment and were not in the habit of managing their excess cash for higher yields. The media focus on Silicon Valley Bank’s failure in March 2023 caused many bank customers to change how they managed their excess cash. This change in customer behavior forced banks with weaker deposit franchises to raise deposit rates to retain customers and deposits.

Banks have deposit franchises with varying degrees of strength. Many different factors can create a strong deposit franchise such as a long history in a marketplace, a strong branch and ATM network, a strong sales culture within the bank of asking for additional deposits from customers, and the size of the bank. Banks with weak deposit franchises use higher rates to attract price sensitive customers.

When Silicon Valley bank failed, the banks with weak deposit franchises had to raise their deposit rates more aggressively to retain their deposits. During Q2 and Q3 of 2023, these banks raised deposit rates to a level that stabilized their customer bases. We estimate this level is about 3.75% to 4.00%. Although these banks have weak deposit franchises, their net interest margins (“NIM”) have already compressed. In a stable rate environment, they should have loans and securities repricing to higher rates as they mature and their NIMs should gradually widen. In a declining rate scenario, they should be able to reprice their deposit rates lower. This will lead to wider NIMs. There is also the possibility that they will strengthen their deposit franchises and attract less rate sensitive deposits. We think this scenario is less likely, but there are a few banks where this is a possibility.

Banks with stronger deposit franchises are experiencing continued deposit cost pressures. They have not had to raise deposit rates as aggressively because their customers are not as price sensitive, however, with money market rates above 5%, even customers of these banks with strong deposit franchises are looking to better manage their excess cash. This has put continued pressure on these banks to retain deposits. Even JP Morgan Chase has not been immune. On its most recent earnings conference call, the CFO said that the bank expects to see continued movements by customers to seek higher deposit rates.

We believe the current high level of interest rate risk will dissipate with time. We believe the inverted yield curve and the significant rate increases by the Federal Reserve is causing the small-to-regional banks to under-earn compared to our estimate of their normalized earnings power. Despite this under-earning, we observe that the small-to-mid-sized regional banks trade at the low end of both absolute and relative valuations. It is a classic value situation of the market assigning a low multiple on stocks with depressed earnings.

New York Community Bank

At the end of January, New York Community Bank (“NYCB”) reported Q4 earnings. The surprisingly bad earnings report caused the stock to decline 37% in one day. The stock has continued to slide despite a $1 billion recapitalization led by former Secretary of Treasury Steven Mnuchin.

NYCB’s poor earnings report and stock price decline in January was a catalyst for the entire regional bank sector underperforming so far in 2024. Through March 31st, the SPDR S&P Regional Bank ETF (“KRE”) was down 3.33% versus the S&P 1500 Financials Sector Index which rose 11.67%. The January earnings season was constructive, but NYCB’s report changed investor sentiment on the regional banks. The question presented to us as bank investors is “Are NYCB’s problems idiosyncratic or systemic to all banks?”

We believe NYCB’s issues are idiosyncratic to NYCB. NYCB has long been a New York City apartment lender. Their track record over many decades has been spectacular with near zero losses. But, in 2019, NYC passed a law that limited how much landlords could raise rents. In the current inflationary environment, landlords’ costs are rising, but they can’t raise rents, so investors are concerned that landlords will get squeezed so much that they will default on their loans.

The NYCB acquisition of Signature Bank highlighted a potential regulatory oversight. NYCB crossed the $100 billion asset threshold, placing it in a new regulatory category with stricter capital requirements. Regulators should have recognized this deficiency in capital and forced NYCB to raise its loan loss reserves and raise additional capital instead of reporting a bargain purchase gain. If regulators were more proactive, the issues with NYCB purchasing Signature could have been avoidable.

We think the regulator's treatment of NYCB was idiosyncratic because of NYCB’s concentration in NYC apartment loans and its crossing $100 billion in assets with the Signature Bank purchase. We think SMID banks underperformed their large bank peers starting on January 31st because of NYCB’s unique issues.

Best Opportunities in Regional Banks

Within SMID banks we group our favorites into three buckets: Puerto Rican banks, growth banks, and small banks with unique stories.

Puerto Rican Banks

Banking in Puerto Rico is an oligopoly. In 2006, there were 11 banks in Puerto Rico and the economy had just entered a recession that would last 15 years. Through bank failures and consolidation, there are just three commercial banks operating in Puerto Rico. We have seen the Puerto Rican banks expand their margins and improve their returns. We also see early signs that bank stock investors are taking note by placing higher valuations on the Puerto Rican banks. We’ve owned First Bancorp and OFG Group for several years and continue to think they have attractive upside.

Growth Banks

We have written about Growth Banks in the past. We continue to like this group of banks. They have cultures that foster organic growth. For banks to grow, they must generate capital through retained earnings. So, many of these growth banks also have high returns on capital. One way to identify these banks is to screen for banks with the highest tangible book value per share growth over a 10-year or 20-year timeframe.

The banks we hold that fall into this category are First Citizens, Western Alliance, Pinnacle, United Missouri, Esquire, Axos, Customers, and Webster.

Small Banks with Unique Stories

We also own smaller banks that have unique stories: NYCB collateral damage (DCOM & CNOB), small cap M&A banks (OSBC, BANC, & BFST), ultra cheap but solid banks (FBIZ, OPBK, & UNTY), and a purchaser of loans from other banks (NBN). While each of these positions is small due to liquidity considerations, we think each will generate attractive returns.

-1.jpeg?width=579&height=579&name=20141211_GCM_0027_edit_web%20(1)-1.jpeg)